Stop Losing Profit: The Contractor’s Guide to Overhead Allocation

Contractor Pain Point

A contractor finishes the year with strong revenue but weak profit.

Jobs looked profitable while they were running. Labor stayed on track. Materials were accounted for. Yet when the year-end financials are finalized, the company profit is much smaller than expected.

This is one of the most common situations contractors face.

The problem is rarely that overhead suddenly increased. The real issue is that overhead was never applied to jobs in the first place.

Most contractors track:

labor

materials

subcontractors

But overhead expenses — things like insurance, office payroll, estimating time, trucks, and shop costs — sit on the Profit & Loss statement without ever being connected to jobs.

When overhead is not allocated, job profitability reports are incomplete and misleading.

A quick way to see whether this is happening in your company is by reviewing the Job Costing Health Report, which helps identify where job cost reporting and company expenses have fallen out of alignment.

This issue ties directly to the foundations explained in Job Costing Basics for Trades & Contractors.

Core Explanation: Why This Happens

Contractors often think of overhead as:

“Expenses that aren’t job costs.”

Examples include:

office salaries

shop rent

insurance

estimating time

software

admin staff

general company trucks

But every job uses these resources indirectly.

Every project requires:

estimating time

scheduling

project management

accounting and invoicing

insurance coverage

office support

If those costs are not spread across jobs, each project looks more profitable than it actually is.

This is why overhead allocation needs to exist alongside the core job costing structure explained in Labor Tracking & Payroll Allocation for Contractors and How to Allocate Equipment Costs in Construction Job Costing.

Some construction projects stop being profitable long before the team is willing to admit it. In Job Can’t Be Saved, contractors can learn the early warning signs that a project has moved from recoverable to financially dangerous — and why delayed decisions usually make losses worse.

Step-by-Step: The Simplest Way Contractors Allocate Overhead

Most construction companies do not use complex allocation models.

Instead, they apply overhead based on field labor activity, because labor is what drives most company overhead.

Visualizing the Overhead Allocation Loop

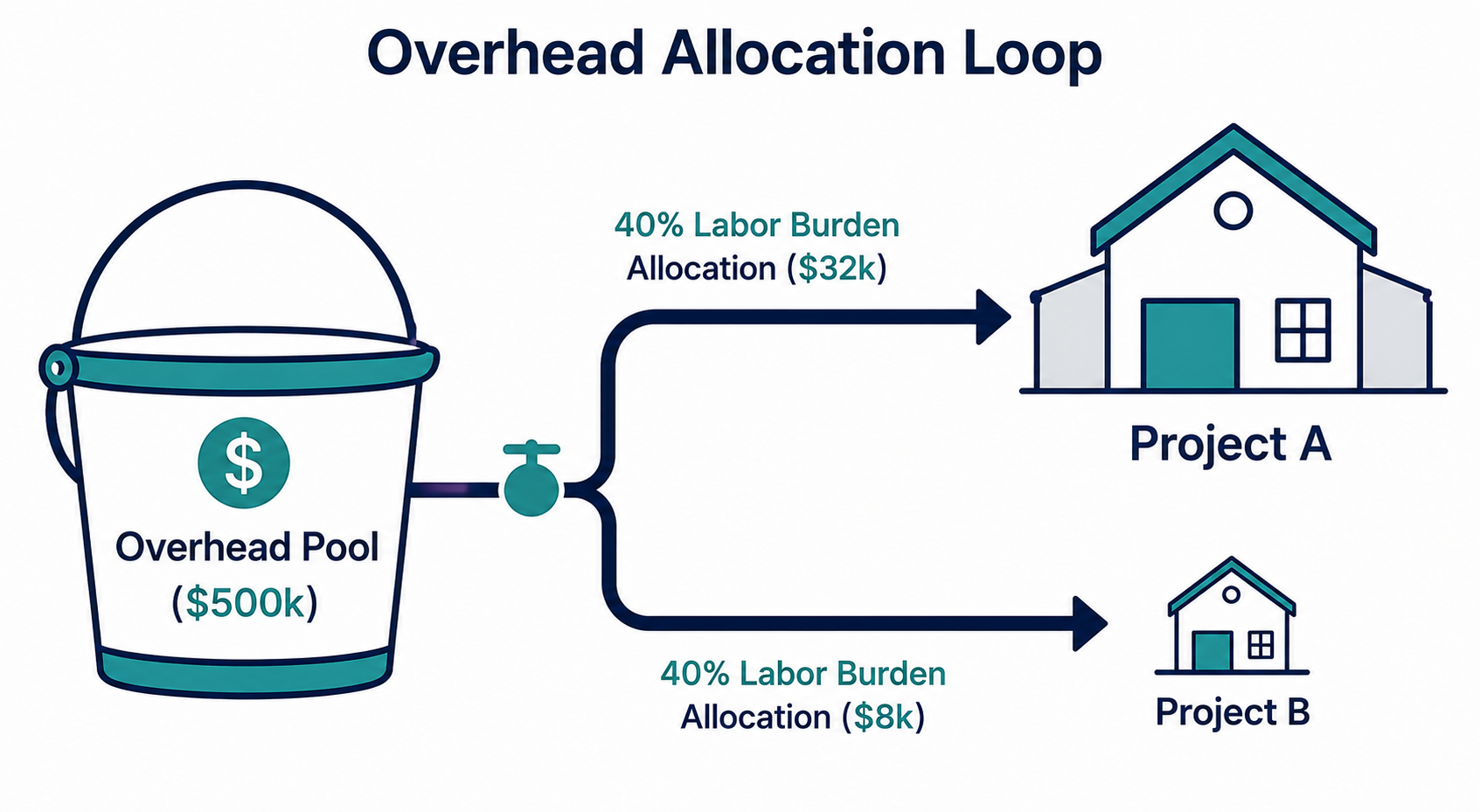

Most contractors make the mistake of leaving overhead as a massive, unassigned bucket of cash at the bottom of their Profit & Loss statement. To run an allocated system, you must "pool" your overhead and distribute it back to active projects using your direct labor hours as the delivery vehicle.

Here is how the data flows from your general company expenses back into individual job cost reports:

1. Calculate Your Total Annual Overhead

Start by totaling everything that is not direct job cost.

Typical overhead includes:

office payroll

rent and utilities

insurance

estimating time

office software

admin staff

shop expenses

general vehicles

Example:

Office Payroll: $240,000

Insurance: $90,000

Rent & Utilities: $60,000

Vehicles & Fuel: $80,000

Software & Admin: $30,000

Total Annual Overhead: $500,000

Why It Matters

This number represents the cost of operating the company, separate from individual jobs.

If you do not calculate this number, overhead usually gets underestimated.

For a quick diagnostic of whether overhead and job costs are aligned correctly, contractors often start with the Job Costing Health Report.

What Goes Wrong If Skipped

Contractors guess.

Many assume overhead is around 10%, when in reality it is often much higher. Benchmarks and ranges are discussed inConstruction Overhead Percentage Benchmarks by Revenue Size.

Strong job costing starts before work begins in the field. How to Create a Job Budget & Stop Repeating Costly Mistakes explains how contractors can build more accurate budgets,improve forecasting, and avoid repeating the same estimating and production issues across future projects.

2. Total Your Field Labor for the Year

Next, calculate your total direct field labor.

Example:

Annual field labor = $1,250,000

Labor is typically used as the allocation driver because labor activity creates demand for:

supervision

scheduling

estimating

office support

3. Calculate Your Overhead Rate

Use this formula:

Annual Overhead ÷ Annual Field Labor = Overhead %

Example:

$500,000 ÷ $1,250,000 = 40%

This means your company requires $0.40 of overhead for every $1.00 of labor performed.

That 40% becomes the overhead rate applied to jobs.

4. Apply the Overhead Rate to Every Job

Now overhead is applied automatically based on labor cost.

Example Job Costs

Labor: $80,000

Materials: $60,000

Subcontractors: $25,000

Overhead Applied

$80,000 × 40% = $32,000

True Job Cost Breakdown

Labor: $80,000

Materials: $60,000

Subcontractors: $25,000

Allocated Overhead: $32,000

Total Job Cost: $197,000

Why It Matters

Now the job reflects the real cost of operating the business, not just direct field costs.

This allows estimating, job costing, and financial reporting to stay aligned.

If your job costing reports still feel disconnected from financial results, the Job Costing Health Reportcan highlight where overhead or job setup problems are creating the gap.

5. Review Your Overhead Rate Periodically

Overhead changes as the company grows.

Examples:

hiring office staff

higher insurance costs

adding trucks

new software systems

If overhead increases but the rate never changes, job profitability reports drift out of accuracy.

That is why most contractors revisit their overhead rate at least annually as part of the financial control process described in Monthly Close Checklist for Contractors (The Control System Most Shops Skip).

Insider Notes: Contractor Gotchas

Owners often forget to include their own salary

Owner compensation is a real business cost and should be included when calculating overhead.

Small jobs consume more overhead than expected

Quick jobs still require:

scheduling

invoicing

coordination

project management

If overhead is not applied consistently, smaller jobs can appear more profitable than they truly are.

Equipment costs are separate from overhead

Owned equipment should be recovered using the system explained in Equipment Cost Recovery Rate Formula for Contractors.

Mixing equipment costs into overhead hides the true cost of equipment usage.

Without clear cost codes, job costing reports quickly become unreliable and difficult to use for decision-making. Why Cost Codes Matter in Budgeting breaks down how organized cost code systems help contractors track labor, materials, and overhead more accurately while improving visibility into where profit is actually gained or lost

Real-World Impact

When overhead allocation is implemented correctly, contractors gain much clearer financial visibility.

Accurate job margins

Jobs show their true cost, not just field expenses.

Better estimating

Estimators price work knowing the real cost structure of the company.

Early financial warning signs

If overhead begins increasing faster than revenue, leadership sees it quickly.

Sustainable growth

Many contractors grow revenue rapidly but lose profitability because overhead quietly expands. Proper allocation prevents this.

If job costing reports still feel disconnected from financial results, running the Job Costing Health Reportis often the fastest way to identify where reporting and job setup systems are breaking down.

Summary

Overhead allocation is not an accounting exercise.

It is a profit visibility system.

Without allocating overhead:

job margins appear inflated

estimating becomes unreliable

profits disappear at year end

A simple labor-based allocation system ensures that every job carries its share of the company’s operating cost.

And when contractors understand their real job costs, they can price work with confidence and protect margin as the business grows.

FAQ

Do contractors really need to allocate overhead to jobs?

Yes. Without allocating overhead, job margins only reflect direct costs like labor and materials. The company may appear profitable at the job level while losing money once overhead expenses are considered.

How does overhead allocation work in QuickBooks?

Most contractors calculate an overhead percentage and apply it during estimating or job profitability analysis. Overhead expenses stay on the company financials while the percentage helps evaluate true job margins.

What happens if overhead is not allocated?

Job profitability reports become misleading. Contractors may believe jobs produce strong margins, while the company struggles financially because overhead expenses were never accounted for.

Is overhead allocation required for construction companies?

It is not legally required, but it is widely considered a best practice for contractors who want accurate job costing and reliable estimating.

When should a contractor update their overhead rate?

Most contractors review and update their overhead rate once per year or when significant changes occur, such as hiring office staff, purchasing additional vehicles, or expanding operations.

Disclaimer

This content is for general educational purposes only and does not constitute tax, legal, or accounting advice. Individual circumstances vary, and tax and reporting requirements can change. Always consult a qualified CPA, tax professional, or legal advisor for guidance specific to your business.